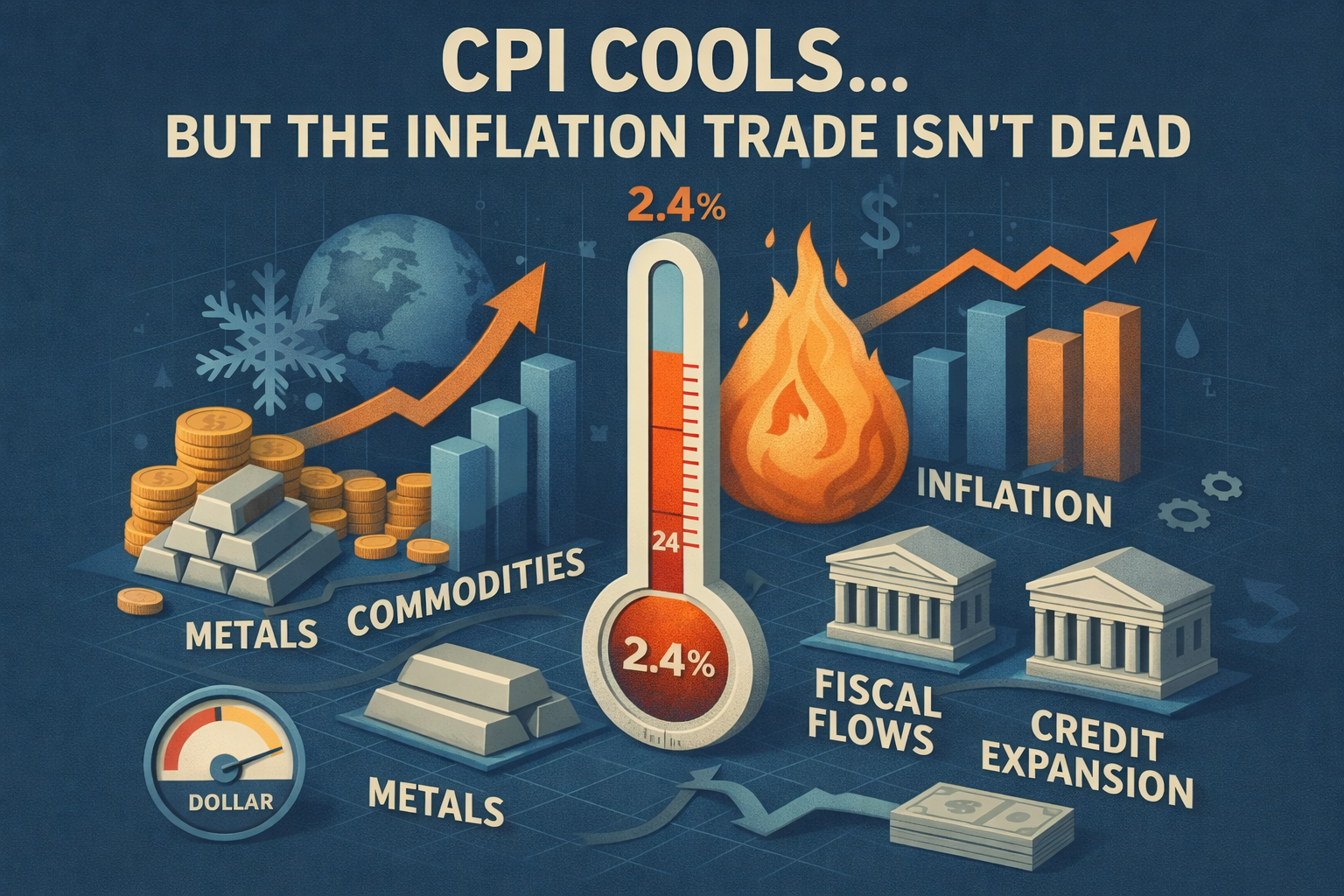

On Friday, we got the January CPI report. Headline year-over-year inflation came in at 2.4%, below the consensus expectation of 2.5%. On the surface, that looks like another step in the “inflation is cooling” narrative that has dominated over the past year.

But I want to explain why I don’t think this print changes the bigger picture—and why, from a business cycle and MMT perspective, we may actually be getting close to the point where inflation starts to reaccelerate.

More importantly, I want to walk through what this means for portfolios and asset positioning. Because if you wait for CPI to clearly turn higher before positioning for inflation, you’re probably already too late.

The Market Isn’t Fully Buying the “Cooling Inflation” Story

Here’s something interesting: even as CPI has cooled over the last year, assets that typically outperform in inflationary environments have been winning.

Think about what’s been working:

- Non-U.S. equities (rest of world) outperforming U.S. stocks

- Materials and metals surging over the past year

- Gold massive rally despite the recent pullback

- The U.S. dollar in a persistent bearish trend

That’s an inflation-tilted portfolio outperforming—even while headline CPI trends lower.

So what gives?

My view is simple: markets often move ahead of CPI. By the time inflation clearly shows up in the official data, the destabilizing phase of the cycle is usually close at hand. The real opportunity—the period where growth and inflation lift asset prices together—comes before CPI spikes.

If you wait for confirmation in the CPI print, you’re likely entering the trade late in the cycle.

The MMT Causal Chain: From Fiscal to Inflation

Let’s walk through the structure of how inflation develops from an MMT and post-Keynesian balance sheet perspective.

Step 1: Fiscal Adds Financial Assets

When the government runs a deficit, it adds net financial assets to the private sector. That fiscal spending becomes:

- Profits

- Income

- Savings

- Investment capital

This is the initial capitalization of the private sector.

Step 2: Credit Expansion Takes Off

Once profits are present, the private sector attempts to capture and expand them. Through endogenous money creation, banks create new loans. That expands:

- The money supply

- Investment

- Balance sheets

This is where the credit cycle accelerates.

We saw a major fiscal push in 2023. By early 2024, bank credit began accelerating again. That’s not coincidence—that’s the transmission mechanism.

Step 3: Asset Prices Rise

As credit expands, asset prices rise to defend expanding balance sheets.

Stocks rising over the past two years? That fits the pattern.

When loans are created to finance investment, new money enters the system. Asset prices must adjust upward to reflect the larger nominal structure of the economy.

Step 4: Output Prices Catch Up

Here’s the critical step.

Eventually, the price of output must rise to justify:

- Higher asset prices

- Higher balance sheet levels

- Higher nominal debt loads

In other words: CPI follows the credit expansion.

Inflation is often the final stage of this expansionary process—not the beginning.

That’s why I believe we’re getting closer to the point where CPI begins pushing higher again. The fiscal impulse of 2023 and the credit reacceleration of 2024 are still working through the system as we enter 2026.

Inflation as a Destabilizer

There’s another important nuance here.

Fiscal spending kickstarts the cycle by providing the necessary savings base for private sector expansion. But inflation eats away at that base in real terms.

Unlike automatic stabilizers (like unemployment benefits), inflation acts more like an automatic destabilizer. It erodes the real value of the fiscal impulse that started the cycle.

As inflation rises:

- Real fiscal support weakens

- Real incomes compress

- Credit conditions tighten

- The cycle eventually rolls over

By the time CPI is clearly high and accelerating, you’re usually closer to the end of the expansion than the beginning.

Portfolio Implications: Don’t Wait for the CPI Print

The big mistake investors make is waiting for CPI confirmation.

By the time inflation prints hot:

- Asset prices have already adjusted

- The destabilizing effects are underway

- The risk-reward profile has worsened

The time to begin tilting toward inflation beneficiaries was when fiscal accelerated and credit reaccelerated—not when CPI printed 3%.

That’s why over the past year we’ve seen outperformance in:

- Materials

- Commodities

- Metals

- International equities

- Dollar weakness

These are consistent with a late-cycle, inflation-leaning environment.

Reading the Latest CPI Print More Carefully

Yes, January came in cooler than expected. But when you dig into the internals, the story isn’t so clean.

Several analysts have pointed out:

- Three-month averages remain elevated

- Certain seasonal factors are suppressing near-term prints

- Data distortions from prior months are still influencing comparisons

The consensus forecast now shows inflation pushing back toward 3% by mid-summer. In other words, even the mainstream outlook expects some reacceleration from here.

To be clear: I’m not suggesting anything improper in the BLS data. I trust the reporting. But “cooler than expected” doesn’t mean “inflation defeated.”

It may simply mean we’re between waves.

The Fed, Rates, and the MMT View

This brings us to policy risk.

From an MMT lens, rate hikes don’t operate the way mainstream theory assumes. Higher rates:

- Increase interest income paid by the government

- Raise the price level of the system

- Require more nominal income to service higher nominal costs

In that framework, rate hikes can actually reinforce inflationary pressures rather than suppress them.

If policymakers respond to a mid-year inflation uptick with renewed hikes, we could see a feedback loop that pushes inflation further than markets expect.

On the other hand, aggressive rate cuts could slow the cycle meaningfully into 2027.

The key variable isn’t CPI—it’s the interaction between:

- Fiscal

- Credit expansion

- Policy reaction

The Real Focus: Fiscal and the Credit Cycle

At the end of the day, CPI is a lagging indicator of deeper forces.

What really matters is:

- Where is fiscal policy headed?

- How is bank credit evolving?

- Is the credit cycle accelerating or rolling over?

Fiscal drives credit.

Credit drives asset prices.

Asset prices eventually force output prices higher.

If you want to stay ahead of the cycle, you follow fiscal flows—not CPI headlines.

Final Thoughts

January’s cooler CPI print doesn’t invalidate the broader cycle dynamics.

We’ve had:

- A major fiscal expansion in 2023

- A credit reacceleration in 2024

- Strong asset inflation for nearly two years

It would be unusual for that sequence not to eventually translate into renewed CPI pressure.

The key is positioning before the CPI spike—not after.

As always: follow the flows.

If you’d like to hear the full breakdown and see the charts discussed in this analysis, you can watch the complete video below.